EU background on the Sustainable Finance package:

Brussels, 13 June 2023

Objectives and overview of sustainable finance

The EU will need additional investments of around €700 billion every year to meet the objectives of the European Green Deal. The bulk of these investments will have to come from private funding.

To address this challenge, the EU has since 2018 put in place three building blocks for a sustainable financial framework:

- The EU Taxonomy, a common dictionary for economic activities substantially contributing to the EU’s climate and environmental objectives;

- Rules on disclosures and reporting for both companies and investors, to ensure proper transparency for all stakeholders; and

- Tools, such as standards and labels for Climate Benchmarks and the EU Green Bond Standard.

The EU sustainable finance framework is beginning to work as intended, facilitating private finance for green and transition investments.

Significant progress has been achieved to date, and many companies and investors are embracing the opportunities of sustainable finance. At the same time, companies are also facing challenges when transitioning to a climate neutral and sustainable economy. These challenges include identifying solutions where green technologies are not yet available, articulating sustainability objectives and actions as part of business strategies, and complying with higher environmental standards.

Complying with the new disclosure and reporting requirements is challenging as well, as the first reporting cycle for companies may raise implementation and usability questions and may require investments into, for example, processing the required information. The Commission is committed to actively supporting this implementation, and to ensure the usability and inclusiveness of the framework for companies of different sizes, business models and with different starting points in the transition.

What’s in today’s package

The package presented today is an important step in strengthening the foundations of the EU sustainable finance framework:

- The Taxonomy Delegated Acts will facilitate investments in more sectors and economic activities that will be recognised as contributing to the EU’s climate objectives. Today’s package also introduces the first ever environmental taxonomy, including activities and associated criteria for four environmental objectives of the Taxonomy Regulation, other than climate.

- The proposal for a Regulation on transparency and operations of environmental, social and governance (ESG) rating providers will ensure that ESG ratings become a more reliable and transparent component of the sustainable finance value chain.

Moreover, the Commission Recommendation illustrates how the sustainable finance framework encompasses transition finance and explains how companies, investors and financial intermediaries can voluntarily use the current sustainable finance framework to finance their transition to a climate-neutral and sustainable economy, with practical examples and explanations.

Finally, the accompanying staff working document on the usability of the EU Taxonomy and the wider EU sustainable finance framework provides an overview of the key pillars of the framework now in place, and takes stock of the recently adopted measures to enhance its usability.

To complete the picture, the forthcoming European sustainability reporting standards (ESRS) under the Corporate Sustainability Reporting Directive (CSRD), currently subject to the public feedback (since 9 June), will enable companies to communicate sustainability information in a standardised way to a variety of lenders, investors and other stakeholders.

Is the package adding to the administrative burden of companies?

The package presented today is an important step towards strengthening the sustainable finance framework. It does not add any new reporting obligations on companies beyond those already established by the Taxonomy Regulation but increases the usability and effectiveness of the framework.

For instance, the Taxonomy Delegated Acts will now include activities and associated criteria for all six environmental objectives of the Taxonomy Regulation and facilitate their reporting thereby allowing new sectors and operators to show their Taxonomy alignment.

Further, the Commission is committed to actively supporting implementation, and to ensure the usability and inclusiveness of the framework for companies of different sizes, business models and with different starting points.

On ESG ratings, companies will get better clarity on the way they are rated and will be able to consider all potential risks and opportunities from their operations and channel investments accordingly.

The Recommendation on transition finance is non-binding and does not impose any new obligations. It is addressed to non-financial and financial companies interested in raising or providing transition finance, and to Member States and supervisory authorities to support awareness and the uptake of transition finance by market players.

The Commission Staff Working Document “Enhancing the usability of the EU Taxonomy and the overall EU sustainable finance framework” summarises the most recent measures and initiatives adopted by the Commission to support stakeholders in their implementation efforts, simplifying complex parts of the framework and addressing the most urgent usability issues. Among these, the Commission has published a number of FAQs documents to clarify and provide further guidance on the application of the taxonomy criteria and disclosures requirements for eligibility and alignment reporting.

How are SMEs affected by the sustainable finance framework and how is proportionality ensured?

The framework is inclusive and proportionate and will enable SMEs to raise finance for their transition while minimising administrative burden.

While non-listed SMEs, in particular micro enterprises, are not subject to mandatory reporting under the EU sustainable finance regulatory framework, some SMEs may be interested in financing green investments and can benefit by using sustainable finance tools voluntarily.

SMEs may need the support of their financing and value chain partners when considering their transition finance needs, and when raising transition finance in practice.

In this context, financial intermediaries are encouraged to consider that SMEs’ capacity to provide detailed information may be limited. Large companies and financial intermediaries are encouraged to apply the principle of proportionality when engaging with SMEs and to exercise restraint when dealing with SME clients that are interested in raising finance for green investments or when requesting information from SME value chain partners.

ESG ratings

What are Environmental, Social and Governance (ESG) ratings?

ESG ratings provide an assessment about the ESG characteristics, exposures to ESG risks or impacts on the outside world of an entity, a financial instrument or a financial product. They are usually provided by specialised ESG rating providers that also offer other types of services, such as ESG data.

There can be different types/categories of ESG ratings, depending on:

- what they assess (aggregated ESG factors, only individual Environmental, Social or Governance factors, or even specific sub-factors, like climate);

- what perspective they assess (risks to the company, impacts on environment and society in general, both risks and impacts or compliance with international principles); and,

- how they carry the assessment (best in class or in absolute terms, quantitative or qualitative assessment).

Who uses ESG ratings and for what purposes?

Investors and benchmark administrators increasingly use ESG ratings as part of their sustainable investment strategies to take into account risks and/or impacts linked to ESG issues. ESG ratings are often used for pre-investment screening (e.g. for the inclusion or exclusion of equities in a portfolio or fund), post-investment analytics (e.g., to rate the ‘sustainability’ of an investment product or fund), for investment integration (e.g. integrating ESG into investment strategies) or for company engagement.

Companies use ESG ratings to look for investment opportunities and to take account of operational risks but also to verify how they perform against ESG factors, as compared to peers.

Therefore, ESG ratings play an important and enabling role for the proper functioning of the EU sustainable finance market by providing important information, for example, for investors’ investment strategies and risk management.

The market of ESG ratings is expected to continue to grow substantially in the coming years, with the changing nature of risks to companies, growing investor interest to meet certain sustainability standards or achieve certain sustainability objectives.

What is the current situation with regards to the ESG ratings market and what are the objectives of the Commission proposal?

The ESG rating market suffers from a lack of transparency regarding the characteristics of ESG ratings, their methodologies and data sources and how ESG rating providers operate. Currently, ESG ratings do not sufficiently enable users, investors and rated entities to take informed decisions as regards ESG-related risks, impacts and opportunities. As a consequence, confidence in ratings is being undermined.

Therefore, the Commission has been working to improve the reliability, comparability and transparency of ESG ratings. The Commission proposal aims to enhance the quality of ESG ratings, by (i) improving transparency of ESG ratings characteristics and methodologies, and by (ii) ensuring increased integrity of operations of ESG rating providers and the prevention of risks of conflict of interest at ESG rating providers’ level.

Since ESG ratings and underlying data are used for investment decisions and allocation of capital, the general objective of the initiative is to improve the quality of ESG ratings to enable investors to make better informed investment decisions regarding sustainable investments. It will also enable rated entities to better manage ESG risks and the impact of their operations. At the same time, we expect it will foster trust and confidence in the operations of ESG rating providers by ensuring that the market operates properly and conflicts of interest can be prevented.

This proposal does not intend to harmonise the methodologies used for the creation of ESG ratings, but to increase their transparency. ESG rating providers will remain in full control of the methodologies they use and will continue to be independent in their choice, to ensure that a variety of approaches are available in the ESG ratings market (i.e. ESG ratings may differ amongst themselves and cover different areas).

What are the main elements of the Commission proposal?

In order to ensure the better functioning of the ESG ratings market and to improve trust from investors and companies, the proposal introduces a number of requirements on the activities of ESG rating providers.

First of all, ESG rating providers offering services to investors and companies in the EU should be authorised and supervised by the European Securities and Markets Authority (ESMA). This will ensure the quality and reliability of their services to protect investors and ensure market integrity.

The proposal also requires ESG rating providers to use rating methodologies that are rigorous, systematic, objective and subject to validation, to ensure the quality and reliability of ESG ratings. ESG rating providers should review ESG ratings methodologies on an on-going basis and at least annually.

The new rules introduce organisational requirements ensuring the prevention and mitigation of potential conflicts of interests. ESG rating providers should ensure that they provide ESG ratings that are independent, objective and of adequate quality.

As regards transparency, ESG rating providers should disclose information to the public on the methodologies, models and key rating assumptions which those providers use in their ESG rating activities and in each of their ESG ratings product. For the same reason, ESG rating providers should provide more detailed information on the methodologies, models and key rating assumptions to subscribers of ESG ratings and to rated entities.

The Commission proposal also provides for a number of measures specific for smaller ESG rating providers to ensure that the rules are proportionate. Such measures should include the possibility for ESMA to exempt smaller ESG rating providers from a number of organisational requirements where they meet certain criteria. In addition, a transitional regime should be introduced for the first months following the application of this Regulation, to facilitate the initial phase of application for smaller ESG rating providers. Finally, supervisory fees should be proportionate to the annual net turnover of the ESG ratings provider concerned.

Taxonomy Delegated Acts

What is the EU Taxonomy and its Delegated Acts?

The EU Taxonomy is a cornerstone of the EU’s sustainable finance framework and an important market transparency tool that helps direct investments to the economic activities most needed for a green transition.

The EU Taxonomy Regulation, which entered into force on 12 July 2020, allows financial and non-financial companies to share a common definition of economic activities that substantially contribute to EU’s climate and environmental objectives, when determining their investment choices. It translates the European Green Deal objectives by defining and classifying economic activities that are aligned with a net zero trajectory by 2050 and the broader environmental goals other than climate.

The Regulation empowered the Commission with establishing technical screening criteria through Delegated Acts. The first Delegated Act, which applies since January 2022, defines the technical screening criteria for economic activities that can make a substantial contribution to climate change mitigation and climate change adaptation. A second Delegated Act, which also applies since January 2022, specifies the content, methodology and presentation of information to be disclosed by large financial and non-financial undertakings concerning the proportion of environmentally sustainable economic activities in their business, investments or lending activities. A third Delegated Act applicable since January 2023 includes, under strict conditions, specific nuclear and gas energy activities in the list of economic activities covered by the EU Taxonomy.

Today the Commission approves in principle a new set of EU Taxonomy criteria for economic activities making a substantial contribution to one or more of the non-climate environmental objectives, namely:

- sustainable use and protection of water and marine resources,

- transition to a circular economy,

- pollution prevention and control,

- protection and restoration of biodiversity and ecosystems.

To complement this, targeted amendments to the EU Taxonomy Climate Delegated Act expand on the list of economic activities substantially contributing to the objectives of climate change mitigation and adaptation. Amendments to the EU Taxonomy Disclosures Delegated Act clarify the disclosure obligations for all the additional activities and provide sufficient time for non-financial and financial undertakings to report alignment of those activities with the EU Taxonomy. The new criteria are based on the recommendations of the Platform on Sustainable Finance, published in March and November 2022.

How long will the scrutiny period by the co-legislators last?

The Commission has today approved in principle the Delegated Acts. Once translated into all official EU languages, they will be formally adopted and then transmitted to the co-legislators for their scrutiny.

The European Parliament and the Council (who have delegated the power to the Commission to adopt this Delegated Act) will have four months (two additional months can be requested) to scrutinise the Delegated Acts, and, should they find it necessary, to object to them.

The Council will have the right to object to them by reinforced qualified majority (which means that at least 72% of MS (i.e. at least 20 MS) representing at least 65% of the EU population are needed to object to the DA), and the European Parliament by a majority of its members (i.e. at least 353 MEPs) in Plenary.

Once the scrutiny period is over and assuming neither of the co-legislators objects, the Delegated Acts will enter into force and apply from January 2024.

What are the activities included in these Taxonomy Delegated Acts?

The Environmental Delegated Act defining criteria for economic activities substantially contributing to one or more of the non-climate environmental objectives of the Taxonomy Regulation includes 35 activities in 8 economic sectors, mainly:

- Environmental protection and restoration activities

- Manufacturing

- Water supply, sewerage, waste management and remediation activities

- Construction and real estate activities

- Disaster risk management

- Information and communication

- Services

- Accommodation activities

The targeted amendments to the Climate Delegated Act define criteria for additional economic activities contributing to the objectives of climate change mitigation and adaptation. They include 12 new activities covering 6 sectors, plus several targeted updates to existing activities in the Climate Delegated Act:

- Transport

- Manufacturing

- Disaster risk management

- Water supply, sewerage, waste management and remediation

- Information and communication

- Professional, scientific and technical activities

What is the impact of the EU Taxonomy on the financial market?

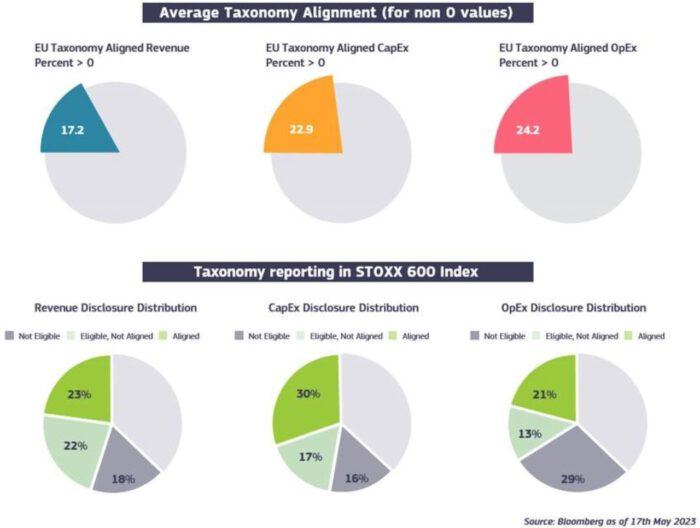

This year’s initial corporate reporting shows encouraging signs that the EU Taxonomy is increasingly being used by undertakings to signal their sustainability performance and efforts. As of 17 May 2023, 63% of companies from the STOXX Europe 600 [1] have already disclosed their taxonomy figures. Among these, 30% (178 companies) reported some levels of alignment with the taxonomy, notably for their capital expenditure (CapEx), 23% (139 companies), their revenue and 21% (127 companies) for their operating expenditure (OpEx). On average, the taxonomy alignment of these companies is around 17% for revenue, 23% for CapEx and 24% for OpEx [2]. Reporting figures also suggest that nearly two in three companies that disclosed Taxonomy-eligible CapEx reported some levels of alignment with the taxonomy and one in two companies that disclosed Taxonomy-eligible revenue reported some levels of alignment with the taxonomy.

How can the EU Taxonomy and its Delegated Acts concretely support green investments?

The EU Taxonomy Environmental Delegated Act approved today delivers an additional set of technical screening criteria for defining activities that contribute substantially to one or more of the non-climate environmental objectives. The inclusion of more economic activities covering all six environmental objectives, and in consequence more economic sectors and companies, will offer new opportunities to scale up sustainable investments.

The EU Taxonomy aims to support investors to finance transition and sustainable projects that substantially improve the environmental performance of activities across all key economic sectors. By clearly defining what is aligned with the EU environmental goals, the EU Taxonomy seeks to encourage companies to launch new projects, or upgrade existing ones, to meet these criteria.

The disclosure by companies of Taxonomy-aligned activities will mean that there is more reliable, comparable sustainability information publicly available on the market for investors and stakeholders. Companies can, if they wish, reliably use the EU Taxonomy to plan their climate and environmental transition and raise financing for this transition. Financial market participants can, if they wish, use the EU Taxonomy to design credible green financial products.

Is there a risk that companies not covered by the EU Taxonomy lose access to financing?

No. The EU Taxonomy is not a mandatory list of activities to invest in, but a tool that facilitates the access of companies to sustainable finance, including for their transition projects.

Banks and investors continue to finance investments in all sectors of the economy but are increasingly integrating considerations of climate transition and physical risks in their financing and pricing decisions.

While the EU Taxonomy can guide market participants in their investment decisions, it does not prohibit investment in any activity. There is no obligation for companies to be Taxonomy-aligned and investors are free to choose what to invest in.

Will the Delegated Acts be revised to include more activities should there be a need?

Yes, in accordance with the Taxonomy Regulation the Commission will regularly review technical screening criteria with the aim to reflect technological progress, new scientific evidence and future EU policy developments. The EU Taxonomy is a living document and will continue to evolve over time, with more activities being added to its scope by means of amendments. For instance, with today’s package, the Commission has included additional economic activities to the list of those contributing to the objectives of climate change mitigation and adaptation.

Moreover, stakeholders will be able to address suggestions and questions on which new activities could be included in the EU Taxonomy or on possible amendments to the technical screening criteria of existing activities. To allow so, the Commission will establish a Stakeholder Request Mechanism and, with input from the Platform on Sustainable Finance, will assess the suggestions.

Will the new Taxonomy Delegated Acts not increase the burden for companies that are already affected by the crisis?

The new delegated acts do not create any new reporting requirements for companies beyond those already established by the Taxonomy Regulation. In accordance with the Taxonomy Regulation and the Taxonomy Disclosures Delegated Act, both already in application, certain large companies are already required to report their Taxonomy alignment.

These delegated acts add a number of new activities and thereby allow companies in several sectors not covered so far to report their Taxonomy eligibility and alignment thus helping those companies to access sustainable finance.

Targeted amendments to the Taxonomy Disclosures Delegated Act are proposed to:

- provide sufficient time for companies to assess compliance with the criteria for new economic activities, and

- facilitate their reporting, in particular in cases where an economic activity may contribute to several environmental objectives (e.g. building renovations substantially contributing to climate change mitigation and circular economy)

Why are certain activities developed by the Platform not included in the Delegated Acts? Will they be included in the future?

The Platform’s reports inform the work of the Commission, but they are of an advisory nature only. They do not bind the Commission on the inclusion of specific sectors and activities in the EU Taxonomy.

The Commission decided to take a two-step approach in developing the Taxonomy Environmental Delegated Act, whereas:

- A first set of activities, for which the proposed technical screening criteria were considered more advanced, was prioritised for adoption in June 2023.

- A second set of activities, for which the proposed technical screening criteria required more time for further assessment in order to comply with the requirements of the Taxonomy Regulation, was postponed for adoption at a later stage.

No timing on the adoption of a delegated act for a second set of activities has been decided yet.

What are the criteria included for aviation (climate change mitigation)?

The Climate Delegated Act already includes a number of activities in the transport sector. In light of the importance to decarbonise air transport, the Commission, following the recommendations of the Platform on Sustainable Finance, decided to include aviation activities, mostly as “transitional” activities for their potential contribution to climate change mitigation. The criteria focus on incentivising the development of zero-emission technologies and the manufacturing and uptake of last generation aircraft that replace earlier models, thus promote fleet renewal with best-in-class fuel efficient aircraft. The criteria also incentivise an increased use of Sustainable Aviation Fuels (SAF). The criteria are ambitious yet achievable. Together, they can thus help mitigate emissions from aviation to a significant degree, before transformative zero-emissions technologies become market-ready and become economically viable alternatives. The criteria will also be reviewed periodically, every three years as for any transitional activities under the Taxonomy Regulation.

What is the Commission planning in regard to the activity of mining?

Mining and refining play a central role in the supply of critical raw materials, which are indispensable for a wide set of strategic sectors including the net zero industry as stated in the recently adopted Critical Raw Materials Act. In order to include mining and refining to ensure greater coherence and a sustainable value chain approach and to achieve the environmental and climate ambitions of the European Green Deal criteria need additional time to be assessed.

The Commission will task the Platform on Sustainable Finance with conducting further analysis on how to include mining and refining of critical raw materials in the EU Taxonomy framework, building on the work of the members in the previous mandate.

Is the EU sustainable finance framework working in practice?

Companies and financial entities have started to apply the tools and disclosure standards for their economic and financing activities. Over the next few years, the quality and availability of disclosures and data will improve as the implementation of the sustainable finance framework progresses, and market actors will be able to leverage the taxonomy and other ESG information to make informed investment decisions, articulate and engage on sustainability objectives and obtain or provide financing for the transition to a climate neutral and sustainable economy.

For instance, early reporting trends show that companies across all key economic sectors are using the EU Taxonomy more and more as part of their transition efforts. For instance, this year’s initial corporate taxonomy reporting shows encouraging trends among large non-financial companies, with many reporting increasing values of taxonomy alignment, in particular in their capital expenditure.

In addition, recent figures on the EU Climate Benchmarks show that the Paris Aligned Benchmarks (PABs) and Climate Transition Benchmarks (CTBs) have been recognised by major investment institutions, including public institutions and non-EU institutions, as a solid tools to help investors tailor their portfolios to follow a decarbonisation pathway. Assets under management of financial products referencing a PAB or CTB benchmark have already reached an estimated EUR 116 billion in 2023.

The benefits from applying the framework will increase with the progressive availability of data. The European Single Access Point (ESAP) will enable digital and open access to that data.

What are the main steps taken by the Commission to improve the usability of the sustainable finance framework?

Enhancing the usability of the Sustainable Finance framework is of key importance to help companies subject to reporting obligations to comply but also to make the use of the framework tools as easy as possible. To address implementation and usability questions, the Commission has adopted a series of measures and initiatives to support stakeholders in their implementation efforts, simplifying complex parts of the framework and addressing the most urgent usability issues. These measures are summarised in the Commission Staff Working Document “Enhancing the usability of the EU Taxonomy and the overall EU sustainable finance framework”.

In addition, the Commission has provided clarity regarding the different sustainability concepts underpinning the framework (i.e. the EU Taxonomy, SFDR and EU Climate Benchmarks) to facilitate their implementation. The SFDR Q&A published in April this year clarified the interactions between the definition of ‘sustainable investment’ under the SFDR and passive funds tracking a Paris-Aligned or Climate Transition Benchmark.

In addition, the Commission published a new FAQ document todayon the interactions between the concepts of ‘taxonomy-aligned investment’ and ‘sustainable investment’ under the SFDR. In this document, the Commission clarified that investments in ‘environmentally sustainable economic activities’ within the meaning of the EU Taxonomy can be qualified as a ‘sustainable investment’ within the meaning of the SFDR. This clarification intends to simplify and encourage the use of the taxonomy framework as a base for a common understanding of what environmental sustainability means in EU financial products and use of proceeds instruments.

The Commission is also working on a comprehensive assessment of the implementation of the SFDR framework. The exercise will mainly focus on assessing any shortcomings of the SFDR to improve legal certainty, and to enhance its usability and role in mitigating greenwashing. The assessment will also consider the interactions with other related sustainable finance legislations, such as the Taxonomy Regulation, the Benchmark Regulation, the MiFID/IDD sustainability amendments and the CSRD.

Enhancing the usability of the Taxonomy and of the wider framework will remain a core element of the Commission’s future work. This involves providing market actors with regular clarifications and guidance, ensuring that the tools are easy to use, that the key sustainability concepts are clear and well connected and that reporting duplications are removed. The Commission will continue to work closely with the Platform on Sustainable Finance and the European Supervisory Authorities (EBA, ESMA and EIOPA) on how to improve the usability and consistency of the rules and tools.

What are the recent measures taken by the Commission to support the implementation of the EU Taxonomy?

The Commission has taken significant steps in supporting stakeholders in implementing the EU Taxonomy. For example, the Commission has published a number of FAQs documents to clarify and provide further guidance on the application of the taxonomy criteria and disclosures requirements for eligibility and alignment reporting. The Commission plans to adopt in due course another guidance document focusing on taxonomy alignment reporting obligations for financial undertakings, which will be required to report their Green Assets Ratio (GAR) and other Key Performance Indicators (KPIs) as of 1 January 2024.

In addition, the Commission has developed a series of online tools to help users better understand the EU Taxonomy in a simple and practical manner, ultimately facilitating its implementation and supporting companies in their reporting obligations. The tools are available on the EU Taxonomy Navigator website and include:

- EU Taxonomy Compass: a visual representation of the economic sectors, activities and technical screening criteria included in the EU Taxonomy delegated acts.

- EU Taxonomy Calculator: an interactive step-by-step guide on reporting obligations for calculating Taxonomy eligibility and alignment ratios.

- FAQs repository: an overview of the frequently asked questions and answers on the EU taxonomy, its delegated acts and disclosure requirements.

With today’s package, the Commission is also publishing the EU Taxonomy User Guide offering a step-by step guide to help non-financial and financial undertakings assess their Taxonomy eligibility and alignment, further exemplified through 12 use cases.

What will be the role of the Platform on Sustainable Finance on usability?

The Platform on Sustainable Finance started its second mandate in March 2023 (after the previous Platform’s mandate naturally expired), with a reinforced focus on advising the Commission on the implementation and usability of the EU Taxonomy and the sustainable finance framework more broadly. Its recommendations will feed into the work of the Commission in this area, but they are of advisory nature only. Therefore, the Platform’s reports do not prejudge any decision or action by the Commission.

More specifically, the Platform has been tasked to deliver recommendations to the Commission to ensure the criteria and disclosures under the EU Taxonomy are usable in practice for all actors in scope. The Platform will also work on developing market practices to better understand how stakeholders are currently using the framework and identifying relevant opportunities and challenges and will advise the Commission on the coherence and effectiveness of the wider sustainable finance framework.

Facilitating transition finance

What is transition finance and what is the Commission doing to encourage it?

Transition finance is about financing private investments to reduce today’s high greenhouse gas emissions or other environmental impact and transition to a climate neutral and sustainable economy. For instance, these could be investments into green production methods or reducing the environmental footprint as far as possible, where no green technologies are yet available.

Transition finance is urgently needed to reduce greenhouse gas emissions by 55% by 2030. It is often needed by companies that want to become sustainable but are not yet there and thus need to do so in steps over time – in other words, companies with different starting points that want to finance their journey towards a sustainable future.

The EU’s sustainable finance toolbox not only supports companies with the highest sustainability records, but also companies with different starting points that have clear sustainability targets. It also allows smaller companies to raise finance for their transition in a proportionate way.

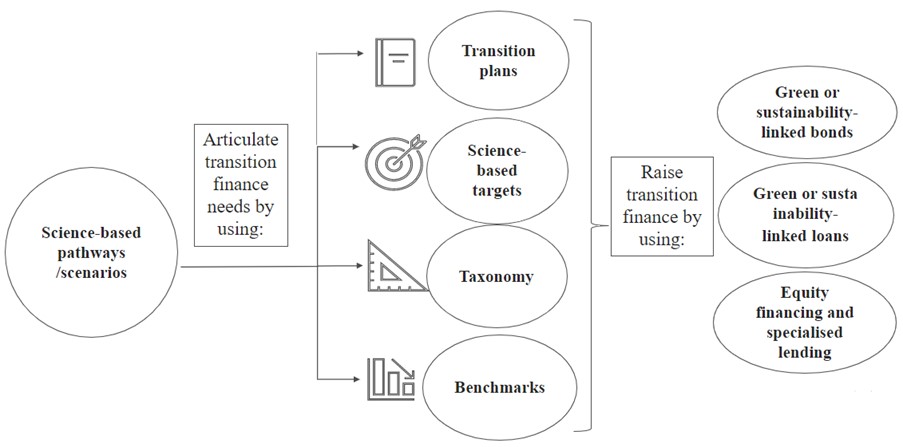

Sustainable finance tools, in particular the Taxonomy, or the EU climate benchmarks as well as credible transition plans can be used to support the definition of transition targets and articulate specific transition finance needs at the level of the undertaking and at the level of economic activities. Transition finance can then be raised through green- or sustainability linked bonds, loans, equity financing or specialised lending.

How can the EU sustainable finance framework help channel investments for the transition?

The EU’s sustainable finance agenda aims to support companies and the financial sector in channelling investments to the transition by encouraging private funding of transition projects and technologies and facilitating financial flows to sustainable investments. The EU has made considerable progress in implementing its sustainable finance agenda over the last 5 years. Milestones include the adoption of the Taxonomy Regulation, the Sustainable Finance Disclosure Regulation (SFDR), EU climate benchmarks in the Benchmark Regulation, the European Green Bond Regulation and the Corporate Sustainability Reporting Directive (CSRD).

The Commission recommendations on transition finance aim to provide guidance as well as practical examples to companies and the financial sector on how they can use the various tools of the EU sustainable finance framework voluntarily to channel the urgently needed investments into the transition and manage their risks stemming from climate change and environmental degradation. The objective is to facilitate transition finance not only for companies that have strong sustainability records already, but also those that are at different starting points, with credible plans or targets to improve their sustainability performance.

Will the recommendations on transition finance place more burden on companies?

The recommendations, as well as transition finance itself, are purely voluntary. Therefore, they will not impose new obligations on companies. They are addressed to companies interested in obtaining transition finance and they offer useful suggestions on how this can be facilitated through the voluntary use of tools such as the Taxonomy, the EU green bond standards or the EU climate benchmarks. Not interested companies can simply disregard it.

For more information

[1] The STOXX Europe 600 index is composed of 600 components representing large, mid and small capitalisation companies among 17 European countries, covering approximately 90% of the free-float market capitalisation of the stock market in Europe.

[2] Data based on FY 2022 disclosures up to 17 May 2023; source: Bloomberg.